Technology Sector Equity Usage Practices

Download a pdf of this article »

While equity compensation is a fundamental component of most technology company compensation programs, balancing the tension between fostering an ownership culture (which serves as a direct link between pay and performance) and managing shareholder dilution can be an ongoing challenge. Further, in recent years, institutional shareholders and their advisors have tightened their scrutiny of share requests for employee stock plans, making it more difficult for companies to “thread the needle” between what shareholders will approve, the need to both fund growth and provide meaningful incentives to executives and other employees, and the pressure of the competitive environment for key talent.

Recently, we examined the equity utilization practices at 150 publicly-traded technology companies spanning the software, hardware and semiconductor sectors with revenues ranging from $50 million to nearly $6 billion, which we call the Tech 150 (see Exhibit A for a list of the Tech 150 companies). Of these companies, 60% are headquartered in California and the other 40% are headquartered across the United States. Data reflect fiscal years ending March 2017 through February 2018. Year-over-year trends are based on data for this same group of companies.

This Thoughtful Pay Alert summarizes the key findings from our analyses and specifically focuses on five key measures of aggregate equity usage:

- Equity vehicle mix;

- Gross burn rate;

- Issued and total overhang:

- Shareholder value transferred (the “fair value” of equity awards granted as a percentage of market capitalization); and

- Stock-based compensation expense.

The definitions of these metrics are provided in Exhibit B to this article.

Five Things That Technology Companies

Should Know About Current Sector Equity Usage Practices

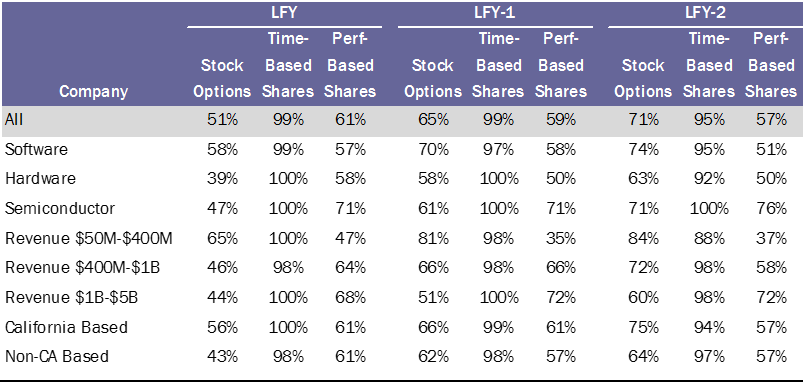

- Equity Vehicle Prevalence. The ongoing decline is stock option usage continues. Only 51% of the companies granted stock options (down from 65% last year). Ninety-nine percent (99%) of the companies surveyed grant time-based RSUs and 61% grant performance-based RSUs (both consistent with last year’s levels).

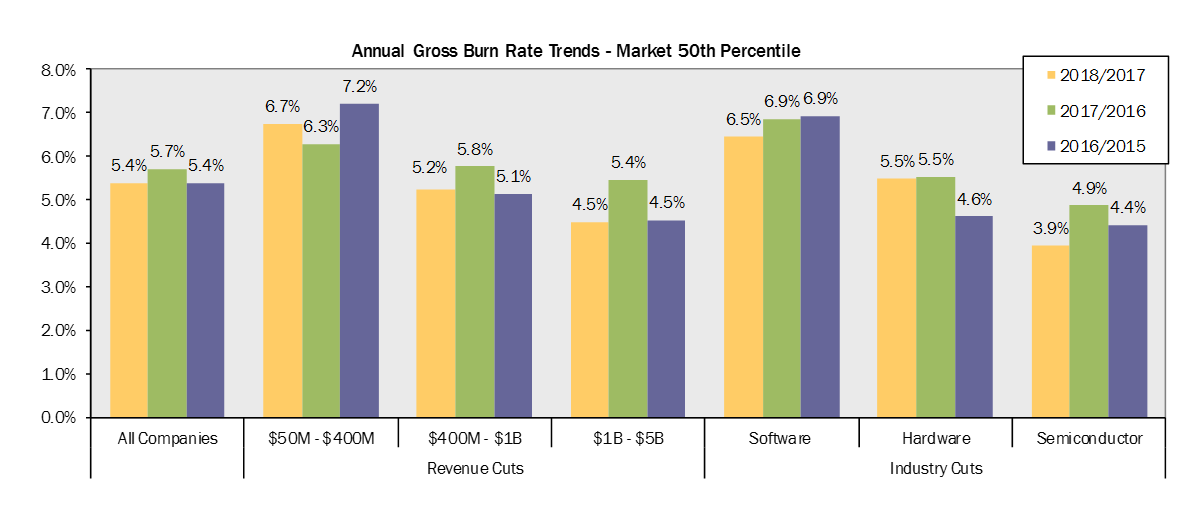

- Burn Rate Levels Declined Year-Over-Year. Burn rate levels declined, compared to increases in each of the past several years (the median year-over-year decrease was 8%). The largest decreases were in the semiconductor and software industry sectors, and among the highest revenue companies.

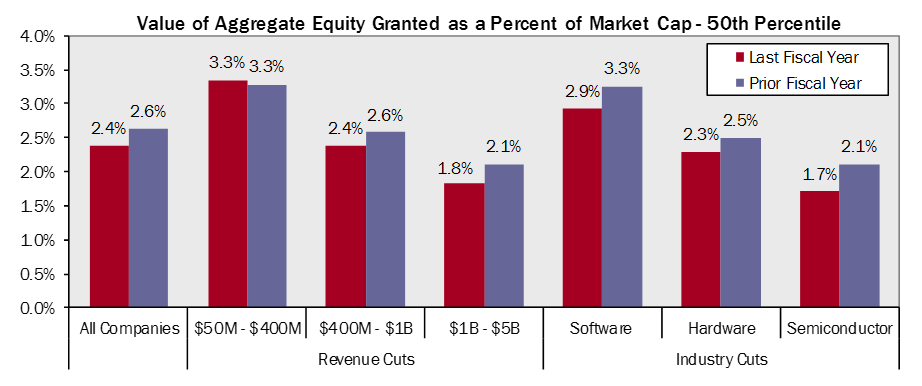

- Aggregate Equity Award Values Increased. The year-over-year grant date fair value of aggregate equity awards increased approximately 14% at the median (with the largest increases in the software and hardware industry sectors). However, values as a percentage of market capitalization decreased approximately 8% at the median.

- Stock Compensation Expense Continue to Draw Attention. With median stock-based compensation expense increasing approximately 16% year-over-year, expect to see increased attention to this measure as shareholders may heighten focus on the use of non-GAAP financial metrics.

- Equity Usage Highest in Software Sector and Among California-Based Companies. The software industry’s and California companies’ focus on equity has not subsided, resulting in the companies showing the highest equity usage under all metrics examined.

Equity Vehicles

Stock option usage among technology companies continues to decline. Only 51% of the Tech 150 companies granted options during the most recent fiscal year reported, down from 65% last year. The number of companies granting performance-based equity awards (61%) now surpasses those granting options. The transition to performance-based awards showed a noticeable increase in the hardware sector but has leveled off in the software and semiconductor sectors. As in past years, companies in the semiconductor sector have the highest prevalence of granting performance shares (71%) while 58% of hardware companies granted performance shares last year (up from 50% in each of the past two years). This shift away from options is the result of several factors, including dilution concerns (given the high number of shares needed to deliver a specified dollar value compared to a full value award), their uncertain effectiveness as a retention tool, and the unwillingness of the major proxy advisory firms to treat them as performance-based awards.

Time-based restricted stock awards (“RSAs”) and restricted stock unit awards (“RSUs”) are almost universal in the technology community, as all but one of the Tech 150 companies grant these full value share awards. RSUs are beneficial to both employees (since they are always “in-the-money”) and companies (since they require fewer shares to deliver the target grant value) making them the most attractive equity vehicle to grant.

The following table summarizes the percentage of Tech 150 companies granting each type of equity vehicle during the past three years.

Gross Burn Rate

Gross burn rate levels declined slightly at the median among technology companies during the most recent fiscal year reported. The overall year-over-year median decrease was 8.0%, with the largest decrease among semiconductor companies (approximately a 16% decrease at the median). The burn rate levels at software companies remain the highest among the three industry sectors, as these companies place a stronger emphasis on equity compensation in the overall pay mix and face pressure to stay competitive in the marketplace. The hardware sector remained constant year-over-year with an approximate burn rate at the median of 5.5%.

Burn rate levels are also correlated with company revenue size and headquarters location. Smaller companies that are growing more rapidly are “spending” more equity (approximately 1.5x that of larger companies) to recruit and retain talent. Cash compensation levels are often more modest as these companies deliver a greater portion of their compensation dollars in equity. Equity is used on a more targeted basis at larger companies to incent and reward employees rather than as a recruiting tool. Similarly, companies headquartered in California have burn rate levels 1.5x those based outside California.

Another contributing factor to the differences in grant practices is the inclusion of an “evergreen” provision in the employee stock plan, which is very common among companies that went public in the last decade. Approximately 37% of the Tech 150 companies (55 companies) have an evergreen provision in their active equity plan that provides for annual replenishments of shares, generally equal to 5% of shares outstanding. Over half (54%) of the companies in the software sector and 63% of the companies with revenue ranging from $50 million to $400 million maintain an evergreen provision. These companies may be able to focus less on managing the share pool and developing strategies to gain shareholder support for more frequent requests.

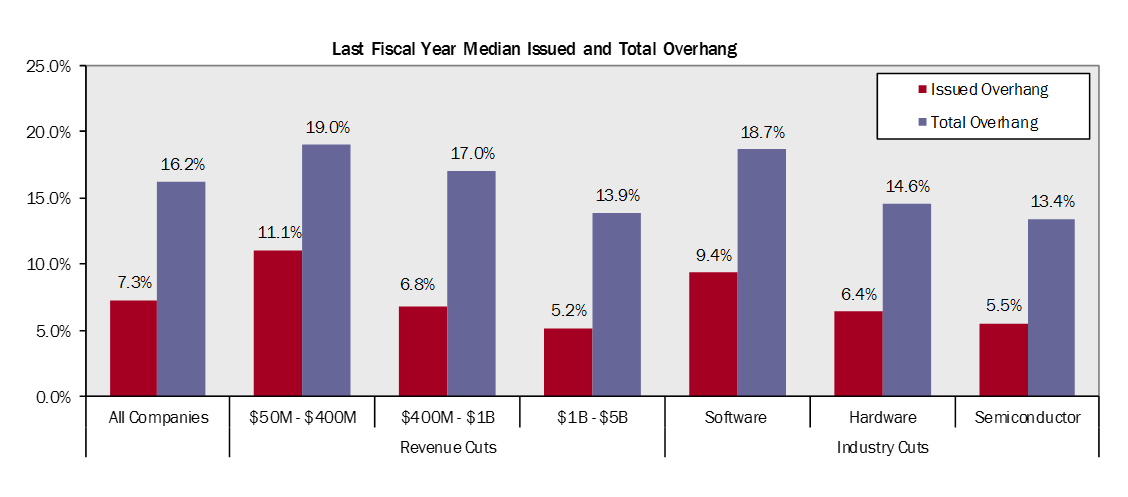

Issued and Total Overhang

Issued and total “overhang” levels have declined in recent years, primarily due to smaller, more frequent employee stock plan share requests and the movement away from stock options. Issued overhang reflects issued/outstanding awards and total overhang also includes shares available for future grant under active equity plans. Previously-granted stock options remain part of a company’s overhang until they are exercised or cancelled, which can be up to 10 years from the date of grant, depending on employee preferences (for example, how long an employee wants to hold the option prior to exercise) and stock market volatility. Conversely, full value share awards are removed from overhang once vested or earned, which generally is no more than four years from the date of grant. Consistent with the higher burn rates associated with active evergreen provisions, companies in the software sector and smaller revenue size companies granting more shares each year see the compounding effect in their issued and total overhang levels. Shareholder Value Transferred (“SVT”)

Shareholder Value Transferred (“SVT”)

Burn rate and overhang measure shareholder dilution on a “number of shares as a percentage of company” basis. Another important measure of dilution is the value of the equity transferred from shareholders to employees through compensatory grants and awards. We refer to this measure as the “shareholder value transferred,” or “SVT.” The dollar value of equity awards granted over the last two years varies significantly by company size and industry, but generally falls between 2.0% and 3.5% when calculated as a percentage of market capitalization. Our review of the Tech 150 showed that, year-over-year, SVT increased for all industry sectors (other than the semiconductor sector) and revenue groupings.

As expected, equity award grant values and SVT for companies in the software sector was approximately 1.75x to 1.9x higher than for the hardware and semiconductor sectors. In addition, SVT for California-based companies was 1.5x higher than companies headquartered outside California.

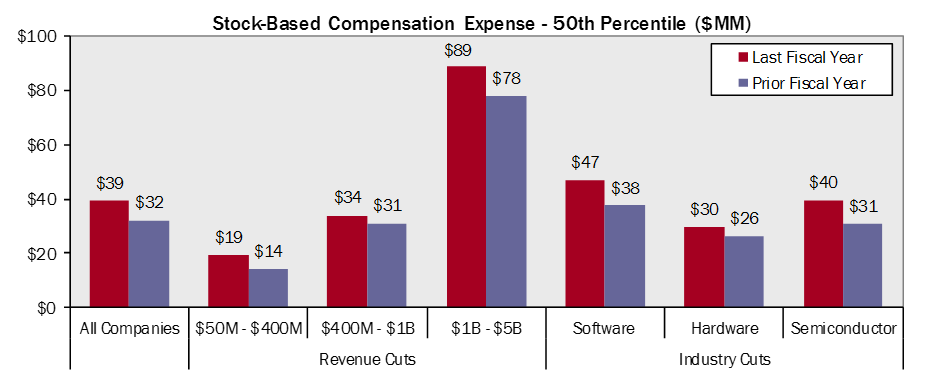

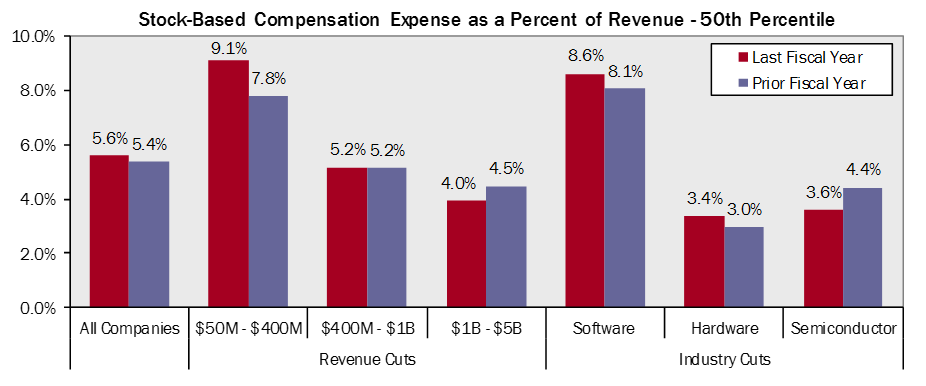

Stock-Based Compensation Expense

Technology companies continue to experience increased scrutiny of the dilutive impact of their equity award grant practices (based on stock-based compensation expense), particularly where top-line growth is slow or modest. This expense has increased year-over-year for most industry sectors and revenue groupings, but declined for the semiconductor sector and for companies with revenues between $1 billion to $5 billion when measured as a percentage of revenue. Stock-based compensation expense not only comes into play with non-GAAP earnings measures, but also impacts free cash flow. In our experience, investors and analysts have increased their focus on these metrics in recent years and typically seek additional relevant disclosure in a company’s public filings.

Final Observations

Final Observations

Setting appropriate target equity usage budgets requires evaluating your equity strategy and the most effective way to use equity awards to recruit, motivate, and retain key executives and employees. This exercise involves a careful evaluation of the form of the awards/vehicles, individual grant guidelines and participation rates by employee group/level and location and the resulting burn rates, shareholder value transferred, and the resulting financial statement impact. With increased scrutiny of employee stock plan requests, as well as the growing use of non-GAAP financials that often exclude stock-based compensation expense, we expect companies will be expected to continue to monitor and manage their equity usage thoughtfully.

About the Authors

The authors of this Thoughtful Pay Alert are Mark Borges and Jason Borrevik, principals at Compensia, and Jodie Dane, a Senior Consultant at Compensia. If you have any questions about this Thoughtful Pay Alert or equity utilization generally, Mark can be reached at 415.462.2995 or mborges@compensia.com, Jason can be reached at 408.876.4035 or jborrevik@compensia.com and Jodie can be reached at 415.462.1985 or jdane@compensia.com.

Need Assistance?

Compensia has extensive experience in assisting companies in designing and managing their employee stock plans, including navigating the expectations of institutional shareholders and their advisors about share usage. If you would like assistance in analyzing your employee stock plan strategy or negotiating the various pressure points in implementing an employee stock plan or a share reserve increase, or if you have any questions on the subjects addressed in this Thoughtful Pay Alert, please feel free to contact Jodie Dane, Jason Borrevik or Mark A. Borges.

About Compensia

Compensia, Inc. is a management consulting firm that provides executive compensation advisory services to Compensation Committees and senior management.