New SEC Rules on Disclosure of Stock Options Granted in Proximity to Disclosure of Material Nonpublic Information to Go into Effect in 2024

Download a pdf of this article »

As part of its recent rulemaking governing insider trading arrangements and the affirmative defense provided by Exchange Act Rule 10b5-1 to trading on the basis of material nonpublic information, the SEC adopted additional rules which will require public companies to provide new disclosure in their annual reports on Form 10-K and definitive proxy statements about stock option grants to executive officers and directors made close in time to the company’s disclosure of material nonpublic information (“MNPI”). These new disclosure requirements will apply to annual reports and proxy statements filed for fiscal years beginning on or after April 23, 2023. Consequently, for companies with fiscal years beginning on or about July 1, 2023, they will need to include this disclosure in their required SEC filings beginning in the fall of 2024. Companies with calendar year fiscal years will need to provide the information in their SEC filings for 2024 made in 2025.

This Thoughtful Pay Alert summarizes these new disclosure requirements along with our initial compliance recommendations.

Background

In adopting the current executive compensation disclosure rules in 2006, the SEC also addressed what was then a growing concern – the timing of stock option grants to executive officers to take advantage of the imminent release of MNPI that could either significantly increase or decrease the market value of the company’s common stock. At the time, stock options were the most popular means for providing executive officers with the opportunity to acquire an equity stake in their company.

Typically granted with an exercise price at the fair market value of the underlying company stock at the time of grant, options are designed to motivate the recipient to work to increase company value, because the optionee only benefits if the company’s stock price exceeds the exercise price at the time of exercise. Timing a stock option grant to occur immediately before the release of positive MNPI (commonly referred to as “spring-loading”) can benefit executive officers with an equity award that would likely be “in-the-money” as soon as the MNPI was made public. On the other hand, if a company is aware of MNPI that is likely to decrease its stock price, it could delay a planned stock option grant until after the release of such information (commonly referred to as “bullet-dodging”).

As part of its significant revision of its executive compensation disclosure rules in 2006, the SEC noted that the existence of a program, plan, or practice to select stock option grant dates for executive officers in coordination with the release of MNPI would be material to investors and should be fully disclosed. Accordingly, many companies began to adopt and disclose their equity award grant policies in their proxy statements; many of which prescribed that equity awards would only be granted at specified times during the year to minimize the risk of “spring-loading” or “bullet-dodging.” However, since there was no specific requirement to separately identify stock option grants that were “spring-loaded” or “bullet-dodging” as part of their CD&As or related tabular disclosure, investors may not have a clear picture of the effect of a stock option that is granted close in time to the release of MNPI on a company’s executive officers’ compensation.

As part of its recent initiative to examine insider trading arrangements, the SEC decided to further address this concern.

New Stock Option Disclosure Requirements

In December 2022, the SEC adopted amendments to its insider trading rules to, among other things, add new conditions to the affirmative defenses to trading on the basis of MNPI in insider trading cases provided by Exchange Act Rule 10b5-1. These amendments are designed to address concerns about abuse of the rule to trade securities opportunistically on the basis of MNPI in ways that the SEC believes harm investors and undermine the integrity of the securities markets. At that time, the Commission also adopted new disclosure requirements regarding companies’ insider trading policies and procedures, the adoption and modification or termination of Rule 10b5-1 plans that are intended to meet the rule’s conditions for establishing an affirmative defense, and certain other similar trading arrangements by executive officers and directors.

While the changes to Rule 10b5-1 generated most of the attention, some significant changes were also made to the SEC’s executive compensation disclosure rules. In particular, the SEC strengthened its disclosure rules applying to equity compensation; particularly stock options, stock appreciation rights (“SARs”), and other option-like instruments that could be susceptible to “spring-loading” or “bullet-dodging.” Thes enhancement are intended to provide more information to investors than is currently available under the existing disclosure rules.

Specific Disclosure Requirements

The SEC added new Item 402(x) to Regulation S-K which, when effective, will require additional specific disclosure involving a company’s use of stock options and similar instruments as part of its executive compensation program. The new rule contains both a narrative and tabular disclosure component.

Narrative Disclosure

Companies will be required to discuss their policies and practices on the timing of awards of stock options, SARs, and/or similar option-like instruments in relation to their disclosure of MNPI, including:

- how the board of directors determines when to grant such awards (for example, whether such awards are granted on a preestablished schedule);

- whether, and if so, how, the board of directors or compensation committee takes MNPI into account when determining the timing and terms of an award; and

- whether the company has timed the disclosure of MNPI for the purpose of affecting the value of executive compensation.

Tabular Disclosure

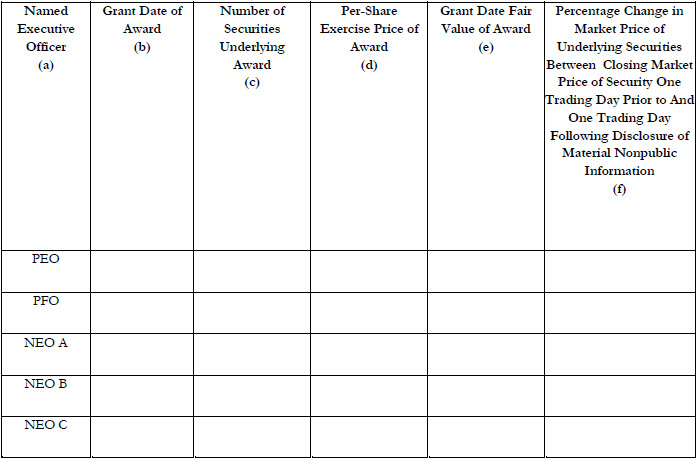

In addition, the SEC is also requiring a new table to highlight for investors stock option grants and similar awards that may be more likely than most to have been made at a time that the board of directors was aware of MNPI affecting the value of the award.

Where, during the last completed fiscal year, a company grants stock options or SARs (or similar option-like instruments) to any named executive officers within the period starting four business days before the filing of a periodic report on Form 10-Q or Form 10-K, or the filing or furnishing of a current report on Form 8-K that discloses MNPI (including earnings information), and ending one business day after a triggering event, the company will be required to include a table containing information on an award-by-award basis for each such award in its annual report on Form 10-K and definitive proxy statement as follows:

Equity Award Table

The grant date fair value of each equity award is to be computed using the same methodology as used for the company’s financial statements under GAAP (and disclosed in its Summary Compensation Table for the last completed fiscal year).

The final rule provides one exception to the enumerated triggering events – if a company files a current report on Form 8-K to disclose the grant of a material new stock option award to a named executive officer (which is to include a brief description of the award), such award does not need to be disclosed in the table (assuming the table is otherwise required). Since this information is already reportable on a Form 8-K, the SEC determined that including it in the required table as well would be redundant and not informative to investors.

In adopting this tabular disclosure requirement, the SEC shortened the period that triggers the tabular disclosure from 14 calendar days before or after a periodic report is filed to five total business days – four days before filing of the enumerated periodic report and one day following the filing.

Smaller Reporting Companies and Emerging Growth Companies

Consistent with the SEC’s approach permitting smaller reporting companies and emerging growth companies to provide scaled disclosure of their executive compensation information, the final rules limit the tabular disclosure to a company’s principal executive officer, the two most highly compensated executive officers other than the principal executive officer who were serving as executive officers at the end of the last completed fiscal year, and up to two additional individuals who would have been the most highly compensated but for the fact that the individual was not serving as an executive officer at the end of the last completed fiscal year.

Compliance Dates

Except as noted in the following paragraph, the new Item 402(x) disclosure requirements do not apply to Exchange Act periodic reports on Form 10-Q and Form 10-K and in any proxy or information statements that are required to include the stock option-related disclosures until the first filing that covers the first full fiscal period that begins on or after April 1, 2023. Consequently, for companies with fiscal years ending on or around June 30th, this means annual filing for fiscal 2024, and for companies with calendar year-end fiscal years, this means annual filings for 2024 made in 2025.

In addition, a smaller reporting company and an emerging growth company are not required to comply with the new Item 402(x) disclosure requirements in their Exchange Act periodic reports on Form 10-Q and Form 10-K and in any proxy or information statements that are required to include the stock option-related disclosure until the first filing that covers the first full fiscal period that begins on or after October 1, 2023.

Thus, these companies generally will have until 2025 to make their initial disclosures.

Observations

While most companies have adopted and observe equity award grant policies that specify when equity awards may be granted by the board of directors, the compensation committee, and/or a management subcommittee designated by the compensation committee, the disclosure of these policies in proxy statements has become inconsistent over time. We expect that companies will immediately begin to disclose their policies in their proxy statements (if they aren’t already), along with a statement that they do not time the grant of stock options or other equity awards to take advantage of MNPI. While new Item 402(x) does not require a company to adopt policies and practices on the timing of awards of stock options, SAR’s and/or similar option-like instruments, or to modify any such existing policies, given the seriousness of this issue, we expect that companies without such policies will adopt an appropriate policy prior to when the new disclosure requirement becomes effective.

Even where an equity award grant policy is already in place, we expect that most companies will review such policies in light of their schedules for filing periodic reports with the SEC to ensure that they have minimized the risk that they will be required to include the required tabular disclosure in their annual report on Form 10-K or proxy statement. Since the filing of current reports on Form 8-K is largely situational, companies may also need to coordinate their equity award grant practices with the likely timing of potential Form 8-K filings; once again to avoid any unnecessary tabular disclosure.

Finally, if a board of directors already considers the timing effects of its equity compensation practices, it will want to make sure that it adequately addresses this subject in its required narrative disclosure. In the rare event that a company triggers the tabular disclosure requirement, it will want to provide a thorough explanation of the circumstances that led to the disclosure and what steps it has taken to minimize the appearance that such action is the result of “spring-loading” or “bullet-dodging.” In sum, the narrative disclosures required by the new rule will not only increase the mix of information available to investors and better inform them of the appropriateness of the company’s equity award practices, but also ensure that investors understand and appreciate the robust nature of the company’s efforts to prevent any insider trading.

Need Assistance?

Compensia has extensive experience in helping companies understand and comply with the SEC’s executive compensation disclosure rules. If you would like assistance in analyzing how the foregoing disclosure requirements are likely to affect your current equity award grant policies and any necessary safeguards to avoid inadvertent disclosure, or if you have any questions on the subjects addressed in this Thoughtful Pay Alert, please feel free to contact Jason Borrevik at 408.876.4035 or jborrevik@compensia.com, Mark A. Borges at 415.462.2995 or mborges@compensia.com, or Hannah Orowitz at (332) 867.0566 or horowitz@compensia.com.

About Compensia

Compensia, Inc. is a management consulting firm that provides executive compensation advisory services to Compensation Committees and senior management.